By Issah Olegor

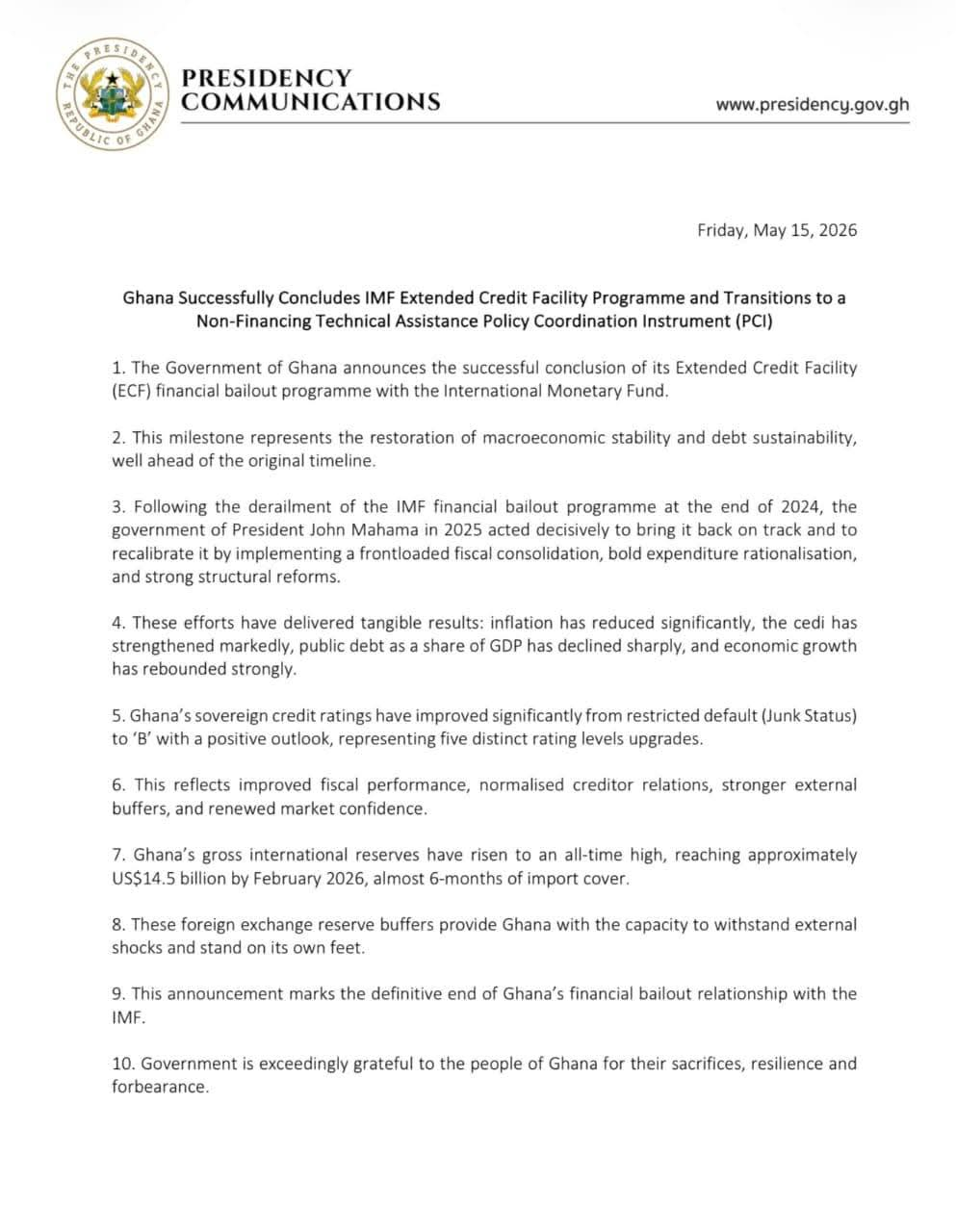

The Government of Ghana has announced the successful completion of its Extended Credit Facility (ECF) programme with the International Monetary Fund (IMF), describing the development as a major milestone in restoring macroeconomic stability and debt sustainability after years of economic turbulence.

The announcement follows the IMF staff’s completion of the 2026 Article IV Consultation and a staff-level agreement with Ghana on the sixth review under the ECF arrangement, as well as a new 36-month Policy Coordination Instrument (PCI) request.

While the IMF acknowledged significant progress made by Ghana under the programme, it also raised concerns about lingering structural weaknesses in critical sectors of the economy and cautioned the government against policy reversals that could undermine recent gains.

In a statement issued by the Presidency Communications Office on Friday, May 15, government said Ghana had officially concluded its financial bailout relationship with the IMF and would now transition into a non-financing technical assistance arrangement under the PCI framework.

According to the statement signed by Presidential Spokesperson and Minister for Government Communications, Felix Kwakye Ofosu, the successful completion of the programme came after the government of President John Mahama undertook decisive economic measures in 2025 to restore confidence in the economy following setbacks that reportedly derailed the IMF programme at the end of 2024.

Government explained that the recovery strategy involved frontloaded fiscal consolidation measures, expenditure rationalisation and the implementation of structural reforms aimed at stabilising the economy.

Officials say those interventions have produced visible results, including a sharp decline in inflation, strengthening of the Ghana cedi, improved economic growth and a significant reduction in public debt as a percentage of Gross Domestic Product (GDP).

The Presidency also announced that Ghana’s sovereign credit ratings had improved from restricted default or “junk” status to a “B” rating with a positive outlook, representing five consecutive rating upgrades.

According to government, the improvement reflects stronger fiscal performance, improved creditor relations, enhanced external reserves and renewed investor confidence in the economy.

Government further disclosed that Ghana’s gross international reserves had reached approximately US$14.5 billion by February 2026, equivalent to almost six months of import cover. It described the reserve build-up as a critical buffer capable of protecting the country against future external economic shocks.

Despite acknowledging the progress, the IMF highlighted several policy concerns that require urgent attention to sustain the gains made under the programme.

One of the major concerns raised by the Fund relates to the balance sheet of the Bank of Ghana.

The IMF noted that losses linked to the Domestic Gold Purchase Programme (DGPP) exposed risks associated with quasi-fiscal activities undertaken by the central bank.

The Fund stressed the need for stronger transparency measures and efforts to shield the Bank of Ghana’s balance sheet from future liabilities arising from the programme. It also recommended that future costs linked to the DGPP be formally recognised in the national budget to improve accountability and oversight.

The IMF further identified the energy sector as another area requiring immediate reforms.

According to the Fund, priority must be placed on reducing distribution and collection losses at the Electricity Company of Ghana (ECG), which continues to face operational and financial challenges that have contributed to persistent instability within the energy sector.

In the cocoa sector, the IMF called for deeper structural reforms to address vulnerabilities threatening the long-term sustainability of the industry.

The Fund specifically urged government to strengthen the legislative framework governing the sector, streamline operational costs and introduce more frequent farmgate price adjustments to improve efficiency and safeguard the financial viability of the Ghana Cocoa Board (COCOBOD).

The IMF also warned that the economic recovery remains fragile and could easily be reversed if fiscal discipline is not maintained. It cautioned against recurring cycles of fiscal imbalances, rising debt levels, weak financial buffers and reform reversals, stressing that maintaining stability after the ECF programme would require consistent policy discipline.

Government, however, expressed confidence that the new Policy Coordination Instrument arrangement with the IMF would help consolidate the gains achieved under the bailout programme without requiring additional IMF financing.

Under the PCI arrangement, Ghana will continue to receive technical assistance and policy guidance from the IMF while using the framework to signal commitment to sound economic management and attract support from private investors and development partners.

The Presidency emphasised that the PCI is not another bailout programme but rather a policy support mechanism intended to strengthen investor confidence, unlock fresh financing opportunities and support the ambition of achieving investment-grade status in the future.

According to government, attaining investment-grade credit status would lower borrowing costs for both the state and the private sector, attract long-term institutional investors, increase foreign direct investment and make financing for infrastructure and private sector development more affordable.

The statement concluded with government expressing gratitude to Ghanaians for their sacrifices and resilience throughout the difficult economic adjustment period.